Leasing is an important way through which companies obtain the tools, equipment, facilities, and resources they need to do business. However, leasing transactions haven't always had a great degree of transparency on balance sheets.

Since a lease has a lasting financial impact, both on the lessors and the lessees, knowing how lease contracts stand between two companies is extremely important.

The new lease accounting standards have been defined to provide greater clarity, transparency, and legal support to companies engaging in lease transactions.

If you are a lessor or a lessee, this article will give you all the information you need to engage in lease contracts.

What is the New Lease Standard?

As per the newly released standards, all lessees and lessors are expected to honestly declare most of the lease transactions they have undertaken during the accounting year in their books of accounts.

The new lease accounting standards apply to all private and public entities engaging in lease transactions. They have been implemented to change the way companies report about leases.

They consist of multiple international standards, which include IFRS 16, ASC 842, GABS 87, and GABS 96.

All real estate, equipment, and vehicle leases, particularly those that last for 12 months or longer, must be declared in the companies’ financial statements to ensure there is compliance with the law which came into effect in many countries in 2019.

Why All the Lease Accounting Changes?

Prior to the implementation of the new lease accounting standards, many companies globally kept leases off their financial records. This created two challenges:

- It made it difficult for parties to ascertain what rights a lessee has over a lessor’s property and how they can use the leased resource.

- It created problems in rental payments and recovering the liabilities owed by the lessee to the lessor.

These challenges necessitated the need for a change in the way lease transactions were reported.

The Creation of IFRS 16 as an International Leasing Standard

Between April 2001 and December 2004, the International Accounting Standards Board (IASB) adopted and issued a variety of standards, such as:

- IAS 17 Leases

- SIC‑15 Operating Leases - Incentives

- SIC‑27 - Evaluating the Substance of Transactions Involving the Legal Form of a Lease

- IFRIC 4 - Determining whether an arrangement contains a lease

These new rules required all lessees and lessors to become more open and transparent about the lease transactions they were engaging in.

These standards came together to form the International Financial Reporting Standards (IFRS) 16 in 2016.

Then in 2019, the ISAB implemented the IFRS 16, which ultimately governs how leasing transactions are recognized, measured, presented, and disclosed in books of accounts.

The IFRS 16 requires companies to identify the specific assets and liabilities for all leases that are longer than 12 months in duration.

The US Brings in ASC 842, GABS 87, and GABS 96

The need for new lease accounting standards became apparent in the United States in 2005.

The Securities and Exchange Commission (SEC) released news that a staggering US$1.25 trillion worth of business was not reported in company balance sheets because they were classified as leases.

This absence of transparency prompted the US Financial Accounting Standards Board (FASB) to bring in three accounting standards – ASC 842, GABS 87, and GABS 96.

- ASC 842

The ASC 842 or Topic 842 requires every public company to report their leasing transactions in their balance sheets if:

- They are reporting their accounting information under the United States Generally Accepted Accounting Principles (GAAP).

- They have leases spanning a duration of 12 months or longer.

- GASB 87

Issued by the Governmental Accounting Standards Board, the GASB 87 requires all companies to list every lease above 12 months duration as liabilities and assets.

- GASB 96

The GASB 96 covers all leases pertaining to Subscription-Based Information Technology Agreements (SBITA), which focus on cloud-based and other technology-subscription-specific leases.

All four standards, which cumulatively make up the new lease accounting standards, require eligible companies to record clearly and in detail the majority of their lease transactions to prevent off-balance-sheet activities.

Ultimately, the goal of the new standards is to ensure that all stakeholders of a company’s financial statements have adequate information about the financial obligations, risks, and rewards pertaining to the leased asset life cycle.

When Did the Standards Come Into Effect?

Both public and private companies have different dates on which the FASB new lease accounting standards went into effect.

For public companies, it was December 15th, 2018, or by January 1st, 2019. For private companies, it was December 15th, 2021, or by January 1st, 2022.

These dates were applicable for both for-profits and non-profits that are public or private, respectively.

Impact of the New Lease Accounting Standards

The implementation of the new lease accounting standards is set to impact companies in three distinct ways:

- Debt Covenants

The new standards will impact how leases are reported and the type of liabilities they ultimately create for the lessee and lessor. Adherence to any debt covenants pertaining to the lease transaction may be impacted as a result.

- Policy Decisions

How a lessor leases out an asset, how a lessee vets and chooses a lessor, and any other decisions regarding the lease, ultimately depend on the leasing policies created by each company.

The new standards will affect what these policies entail, how they are revised/updated and how future leasing policies will be established.

- Lease Processes and Controls

The new standards expect a great degree of information about exactly how lease transactions play out in every site/location where the asset is used.

Therefore, companies will need to record in detail all processes related to the leased asset and create controls that govern all leases organization-wide.

More centralized documentation needs to be created for easier compliance with the standards.

Does Your Company Come Under the New Lease Accounting Standards?

In order to understand how your company may be impacted by the new lease accounting standards, it is important to know how ASC 842 defines the term “lease.”

According to ASC 842, a “lease” is defined as a “contract.” In turn, ASC 842 defines the following – “A contract is or contains a lease if the contract conveys the right to control the use of identified property, plant, or equipment (an identified asset) for a period of time in exchange for consideration.”

Additionally, in order for this particular definition to be applicable to a company that engages in a leasing transaction, two distinct requirements must be met:

- The “identified asset” must be recognized according to the following tenets –

- The “asset” must be specified implicitly or explicitly in the contract.

- The “asset” must be physically distinct.

- The lessor does not have the right to substitute the defined “asset” for another when discharging their duty towards the lessee.

- The “control” over the asset exists only when it meets these tenets –

- The lessee has the complete right to directly use the identified asset.

- The lessee has the full right to receive substantially all of the economic benefits gained through the use of the asset which has been leased.

All leasing transactions that fit the above description are required under the new lease accounting standards to be reported (especially those longer than 12 months).

(Image Source)

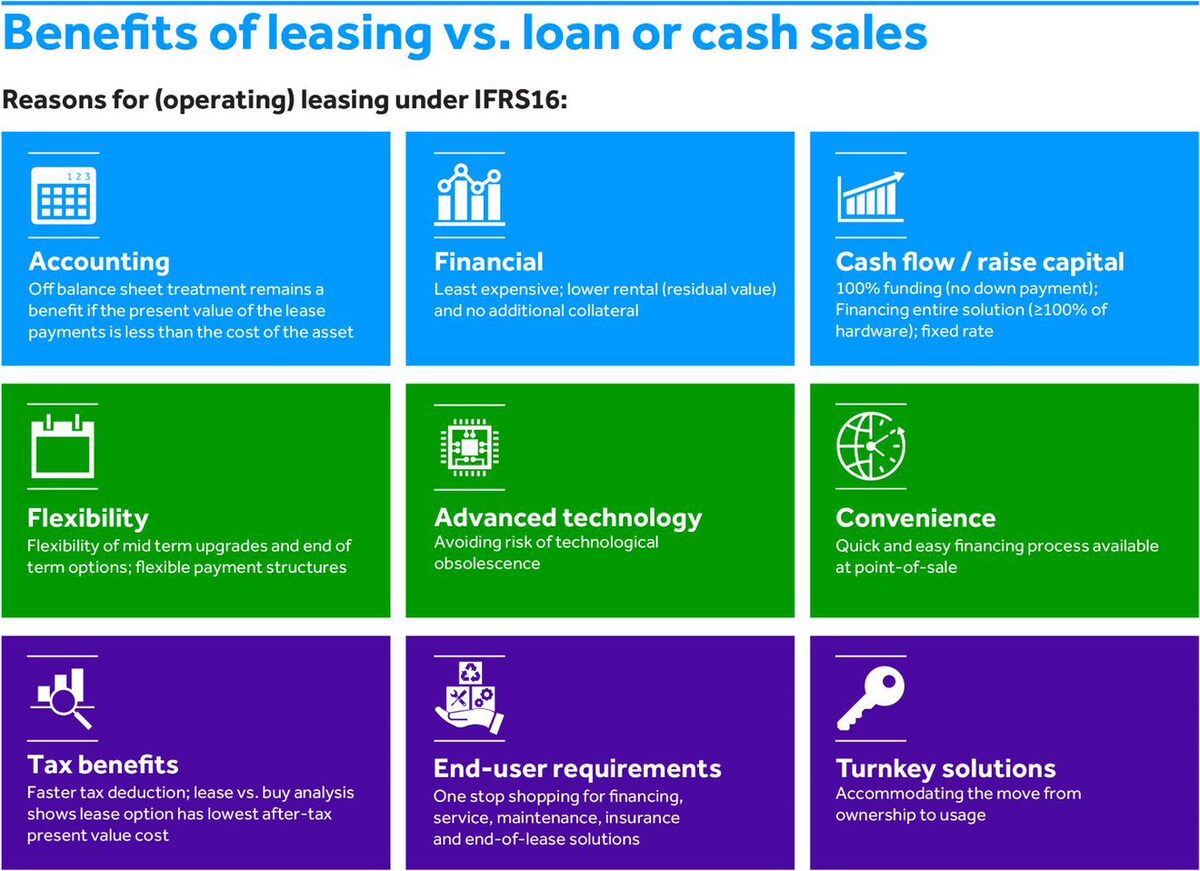

Financial vs. Operating Leases

Most commercial leases fall within two categories - financial leases and operating leases. The IFRS defines what can be termed as finance leases and operating leases.

Financial leases are leases where, for the duration of the lease, both the risks and rewards associated with the lease, are transferred to the lessee.

Operating leases are leases where, for the duration of the lease, both the risks and rewards associated with the lease, remain with the lessor.

In order to differentiate between the two, the IFRS asks companies to consider the following criteria:

- Term of lease – Financial leases are for long-term; operating leases are for short-term.

- Ownership status of a leased asset – In financial leasing, the ownership of the asset transfers from the lessor to the lessee at the end of the contract. But in operating leasing, the ownership of the asset remains with the lessor at the end of the contract.

- Option to purchase the asset – In financial leases, the lessee has the option to purchase the asset at a lower price than the current market value. In operating leases, no such option to purchase the leased asset is offered to the lessee.

- Specialized asset use – In financial leases, the asset leased is specialized and has no other use than the current use. In operating leases, the asset is versatile and has more uses than the one for which it has been leased.

- Net present value (NPV) – The NPV of the minimum lease payments either equals or exceeds at least 90% of the value of the identified asset at the start of the lease. Any lease that does not meet these NPV criteria falls under an operating lease.

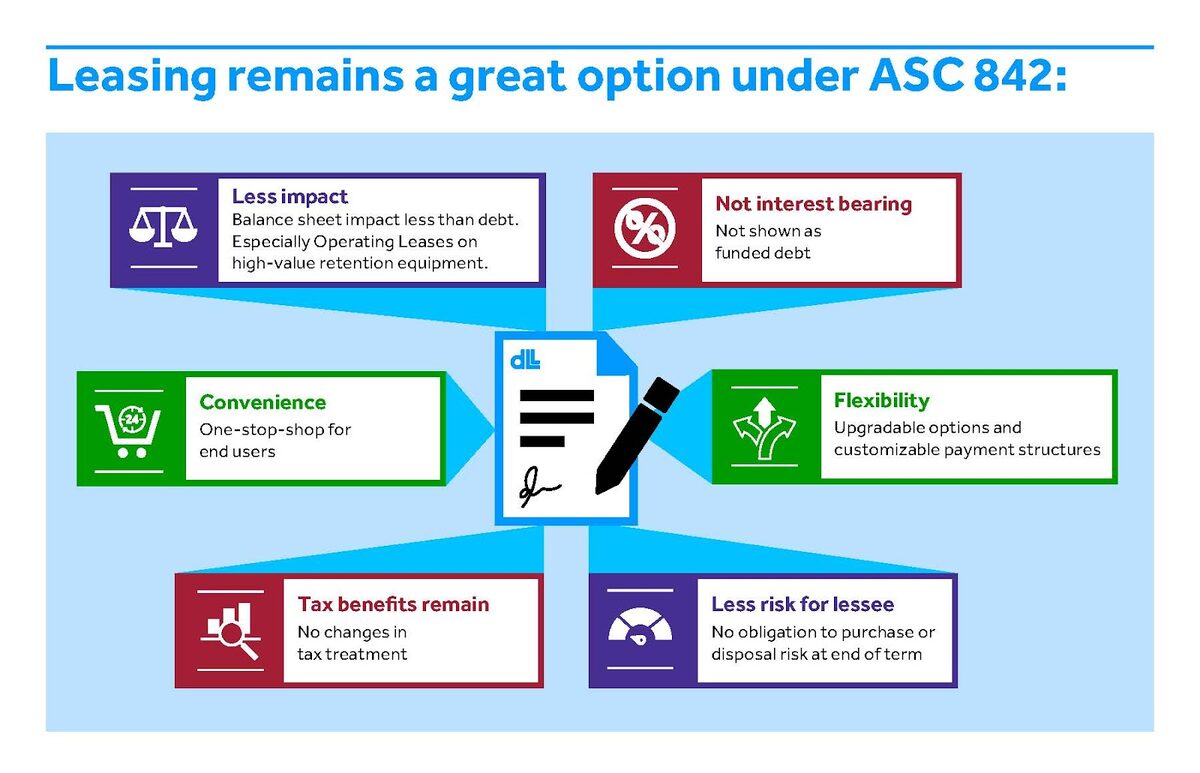

Scope of Coverage

Under ASC 842, the following types of leases come within the scope of the new standards:

- Operating leases

- Financial leases

- Lessor accounting

- Leveraged lease agreements

- Sale-leaseback transactions

While a vast majority of lease contracts between companies fall within the purview of the above five categories, there are some exceptions to the standards. Here is a list of lease transactions that do not fall within the scope of ASC 842:

- Leases pertaining to assets mentioned under ASC 330 (Inventory).

- Leases pertaining to intangible assets (any that don’t fall under the SBITA).

- Leases pertaining to biological matter such as livestock, wildlife, timber, etc.

- Leases pertaining to assets that are still being developed or are under construction.

- Leases pertaining to the use or exploration of non-regenerative natural resources.

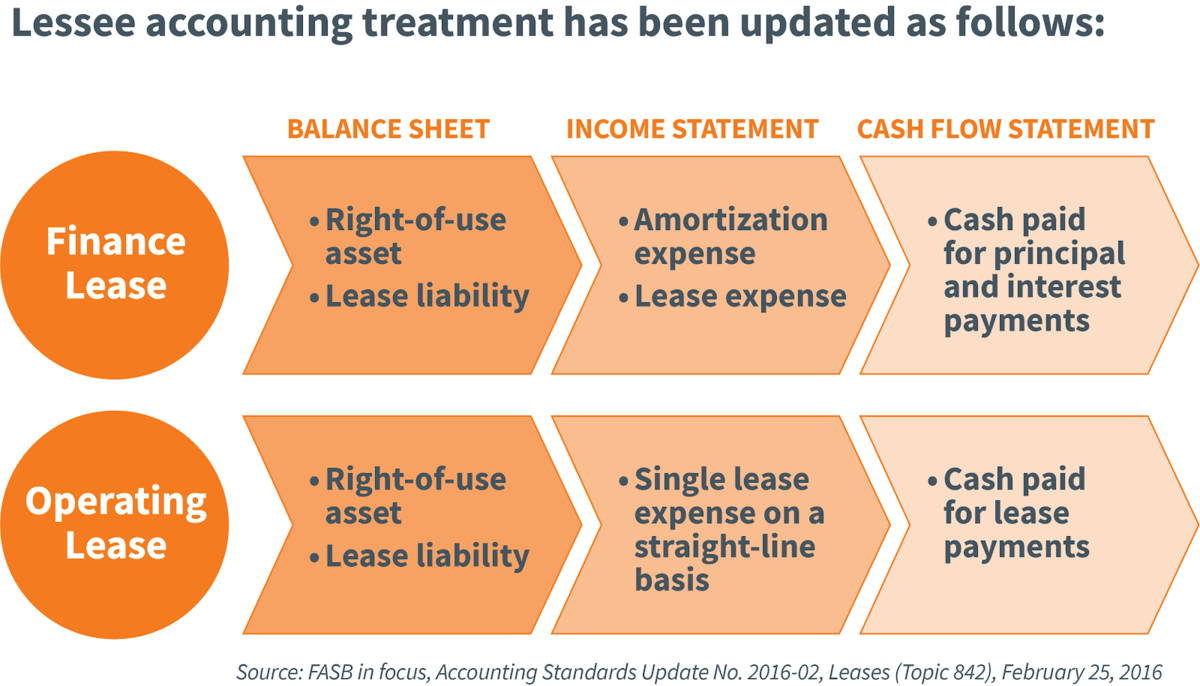

What Changes are Required of Companies?

The lease accounting changes that are expected to be reflected include the following:

- Changes in Balance Sheet Reporting

The company’s balance sheet is expected to also record:

- Operating lease right-of-use (ROU) assets

- Operating lease liabilities

- Finance lease ROU assets

- Finance lease liabilities

- Changes to Ratio Analysis

The new standards may affect the amount of debt a company shows on its financial statements while simultaneously not impacting the company’s equity.

Reporting changes in ratio analysis can give stakeholders a better idea of the company’s performance.

- Application of Practical Expedients

Practical expedients can help the lessee reduce the complexity of the transition to the new standards by providing certain leeway in reporting their lease transactions. These expedients typically apply to:

- Expired transactions

- Transactions where information/documentation is very hard to find

- Impact of past data on current financial information

Depending on their specific eligibility to apply these expedients, companies may be allowed to use either full or modified retrospective approaches.

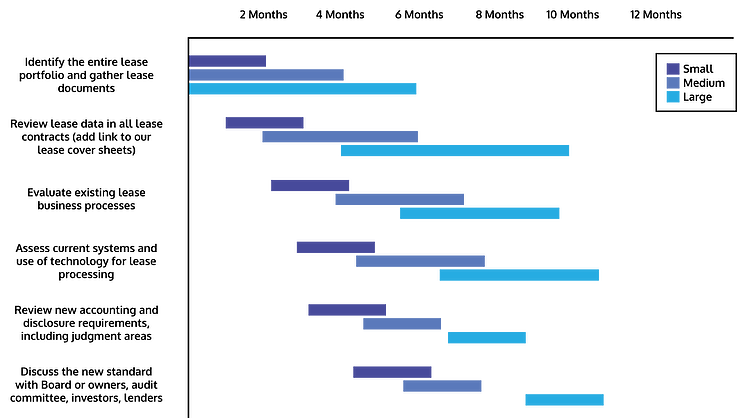

New Lease Standard Implementation Timeline

The time it can take to implement the required accounting modifications to accommodate the new lease accounting standards can differ based on how many leases your company holds.

Let’s say we categorize companies in the following manner:

- Under 100 leases – Small company

- 100 to 2000 leases – Medium company

- Above 2000 leases – Large company

Now let’s consider the steps involved in meeting the new standards:

- Study your complete lease portfolio thoroughly.

- Review lease documentation to narrow down contract details.

- Go through all lease processes, controls, debt covenants, and governing policies.

- Identify and map how each lease is processed and which technology implements the lease transactions.

- Understand the requirements of the new lease accounting standards and consult a CA to know your accounting responsibilities.

- Bring all stakeholders – Board of Directors, investors, creditors, C-suite employees, accountants, etc. – to discuss future steps to comply with the new standards.

Now let’s assume that it takes at least 1, 1.5, and 2 months respectively, for each of the three categories of companies to implement the changes required as per the new lease accounting standards.

Considering the above criteria, it can take companies a minimum of this much time to implement the new accounting:

- Small company – 6 months

- Medium company – 9 months

- Large company – 12 months

Of course, these times may be different for your company, depending on your unique lease administration needs.

In Conclusion

Implementation of the new lease accounting standards can be challenging, especially when you don’t have a centralized database that can help you manage all lease agreements with care.

It helps to have a flexible and customizable lease management platform, which can support your company’s transition to the new standards.

That’s where LeasO comes in.

LeasO's Lease Management software is already fully-compliant with tools that allow you to effortlessly comply with IFRS 16 and other new lease accounting standards. Get in touch with us today to see how it works.