Commercial real estate (CRE), like many others, has its own jargon that can sometimes be challenging to understand. The term "lease amortization" is one of such numerous CRE terms.

Amortizing a lease is the procedure of paying off a debt gradually through a series of payments scheduled at regular intervals. Although it can be challenging, many CRE professionals are tasked with doing just that. Let's talk about the lease amortization schedule and how to handle its intricacies.

What is Lease Amortization?

Lease amortization refers to the process of repaying an operating or finance leased asset over the course of time.

Real estate professionals employ a lease amortization schedule in order to amortize the principle of the lease over the lease term utilizing projected payments calculated on a straight-line basis for lease expenses.

The creation of the journal entries in accordance with ASC 842 requires that professionals have a working knowledge of how to compute their lease amortization schedules.

A simple definition of amortization would be a value reduction of an intangible asset over time. It is the process of lowering the worth of an intangible asset that is included in a lease agreement by taking into account its historical cost, economic lifetime valuation, and residual value.

As a result, the overall debt that is associated with the asset is brought down, also known as amortized, each month.

How is Lease Amortization Calculated?

Based on whether someone has a financing lease or an operating lease, the lease amortization gets calculated separately if their books are prepared in accordance with FASB ASC 842.

Following GASB 87 and IFRS 16, there are no operating leases; instead, all leases get classified as financial leases.

A finance lease operates in a manner similar to the acquisition of the leased asset due to the specifications of the lease. In this case, an interest expense must be taken into consideration for the outstanding lease liability.

Only the lease expense that could be broken down in a straight-line fashion is taken into account for operating leases.

The amortization expense can be regarded as a "plug" number concerning operating leases. A "plug" here implies a placeholder value reported till an accurate estimate can be determined. Although it is not a typical occurrence in accounting, it is the case here.

After the accounting professionals have completed the process of balancing the credits and debits, all the figures get computed, and the remaining is the amortization expense.

When performing the calculations for any reporting period, one should always begin with the lease liability, which represents the current value of all prospective lease payments. The ongoing monthly liability gets utilized when determining the interest expenditure incurred (for finance leases).

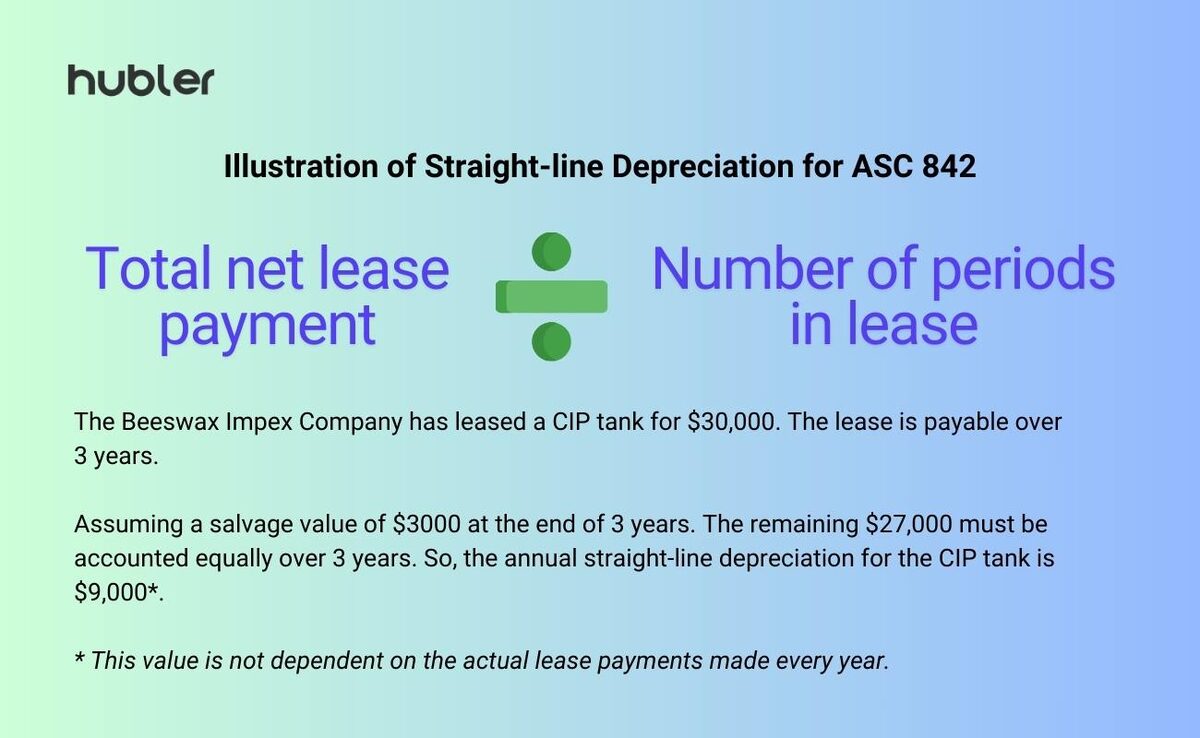

The lease expense can be determined using a simple straight-line method for ASC 842 using all of the lease payments made over the length of the lease (calculated at the lease commencement). See the following illustration:

The initial lease liability is added to the original direct costs and then subtracted from any incentives that were obtained to get at the initial right of use (ROU) asset.

After that, the value of the ROU asset gets reduced, also known as amortized, on a monthly basis up to the final payment. If there's no value for the residual asset, the ROU asset value will be equal to zero.

What is a Lease Amortization Schedule?

A lease amortization schedule is a tabular representation of information that details each of the lease payments, in addition to interest and amortization computations, often on a monthly basis, throughout the length of the lease.

Lease schedules are frequently drafted at the start of a lease because their primary function is to serve as a reference for estimating payments that will be made throughout a lease.

For the duration of a lease, for example, an accountant would frequently use a lease amortization schedule as a point of reference to verify that all payments, interests, and amortization are accurately shown on the company's financial statements.

How to Create a Lease Amortization Schedule?

To create a lease amortization schedule template, include the following data sets:

- Measurement Date - It is the date of lease commencement or ASC 842 effective date.

- Lease Term (in months) - It returns the total number of months for the lease term and influences how the ROU asset gets amortized.

- Lease Expiration Date - It indicates the end of the lease.

- Discount rate - It depicts the annual/monthly incremental borrowing rate.

- Initial direct costs - The costs associated with a lease that would not have come to force had the lease not been executed.

- Prepaid rent - Any rent paid in advance to the lessor before the start of the lease.

- Incentives - One way to get a potential lessee to sign a lease is to offer them attractive incentives like a Tenant improvement allowance (TIA).

- Periodic payments - These govern whether or not payments be made at the start or conclusion of a specific period. Interest expense and the present value of lease payments get calculated accordingly.

- Lease classification - This parameter controls the lease's expense identification structure and the way the ROU asset gets amortized/reduced over the lease's term.

When the lease gets classified as an operating lease, the lessee obtains the rights to make use of the leased asset, but the transaction does not reflect in the lessee's balance sheet.

On the other hand, when classified as a finance lease, the asset gets passed from the lessor to the lessee along with the risks associated, and the asset must get reported on a balance sheet.

How to Calculate the Monthly Lease Liability Amortization Schedule?

Let's delve into a step-by-step procedure to understand this better.

1. Create columns in the spreadsheet

Make five separate columns in the spreadsheet. Date, Lease Liability, Interest, Payment, and Closing Balance are the headings for the respective columns.

2. Insert the due dates and payment amounts

This data comes straight from the lease arrangement. Let's consider a case where there are 12 monthly payments due at the end of each month. We calculate the opening balance of the lease liability for every month.

3. Apply the NPV function

The rate (discount rate) is an input into the Net Present Value (NPV) formula.

Usually, in such a case, the discount rate gets calculated by dividing the total number of payments over 12 months. To get a marginally more precise NPV, one can use this solution.

The NPV function ignores the date of the payments. A present value calculation is not required for the initial payment if it has already been received in advance.

4. Calculation of interest on the lease liability

Since the payments are made monthly, the discount rate has indeed been split by 12 to be congruent with the NPV formula and then applied to the lease liability amount.

5. Determine the Closing Balance

Determine the closing balance of the lease liability at the end of the first month.

6. Carry forward the closing balance to the next period

The preceding month's closing balance should be utilized because it will serve as the opening balance for the subsequent month.

7. Insert each row's formulas

The lease liability's closing balance should resolve to zero at the lease's end. Verify that the formulas are selecting the right cells. If they aren't, that would explain why the amortization schedule for the lease liability isn't decreasing to zero.

In principle, there shouldn't be any interest accrues made in December as the lease liability should get settled.

How to Get an Amortization Schedule?

As evident, creating a lease amortization schedule in a spreadsheet is complicated.

If you manage more than a handful of leases, it may be better to find a lease management software. ASC 842 can be especially complex when contracts are modified. The right software can prevent tedious manual effort and errors in generating your lease amortization schedule.

We recommend a no-code lease management application. While many lease management applications exist in the market, a no-code solution will enable you to integrate and automate upstream and downstream workflows related to your leases and lessors. For example, imagine seamlessly onboarding and approving a lease contract, generating payment advises every month on invoice receipt and verification, and creating automated journal entries that comply with ASC 842 (or IFRS). No-code makes this type of orchestration possible, enabling you to reduce software spend while solving issues across your finance, accounting, and operations workflows.

With a no-code lease management software, you can create speedier audit footnotes thanks to automated quantitative disclosures. Additionally, FASB, GASB, and IFRS policy election templates get simplified, along with the ability to integrate with your existing ERP or accounting software.

So try them out!

Final Thoughts

The identification of the right assets to include and collecting the various elements of value-related data and info to be utilized is the most challenging part of lease administration and consumes the most time when constructing a lease amortization schedule.

The only things that must be done after a lease is finalized are related to keeping track of the lease, renegotiating the terms, and renewing the lease.